SDG Indicator 12.6.1: Number of companies publishing sustainability reports

1. Key features and metadata

Definition: This indicator measures the number of companies reporting sustainability information.

| Sub-indicator | Disaggregated by |

|---|---|

|

EN_SCP_FRMN Number of companies publishing sustainability reports with disclosure by dimension, by level of requirement (Number) |

Type of activity |

Sources of information: National and international companies through ESG rating platforms and global report aggregators then analyzed by the Custodian Agencies.

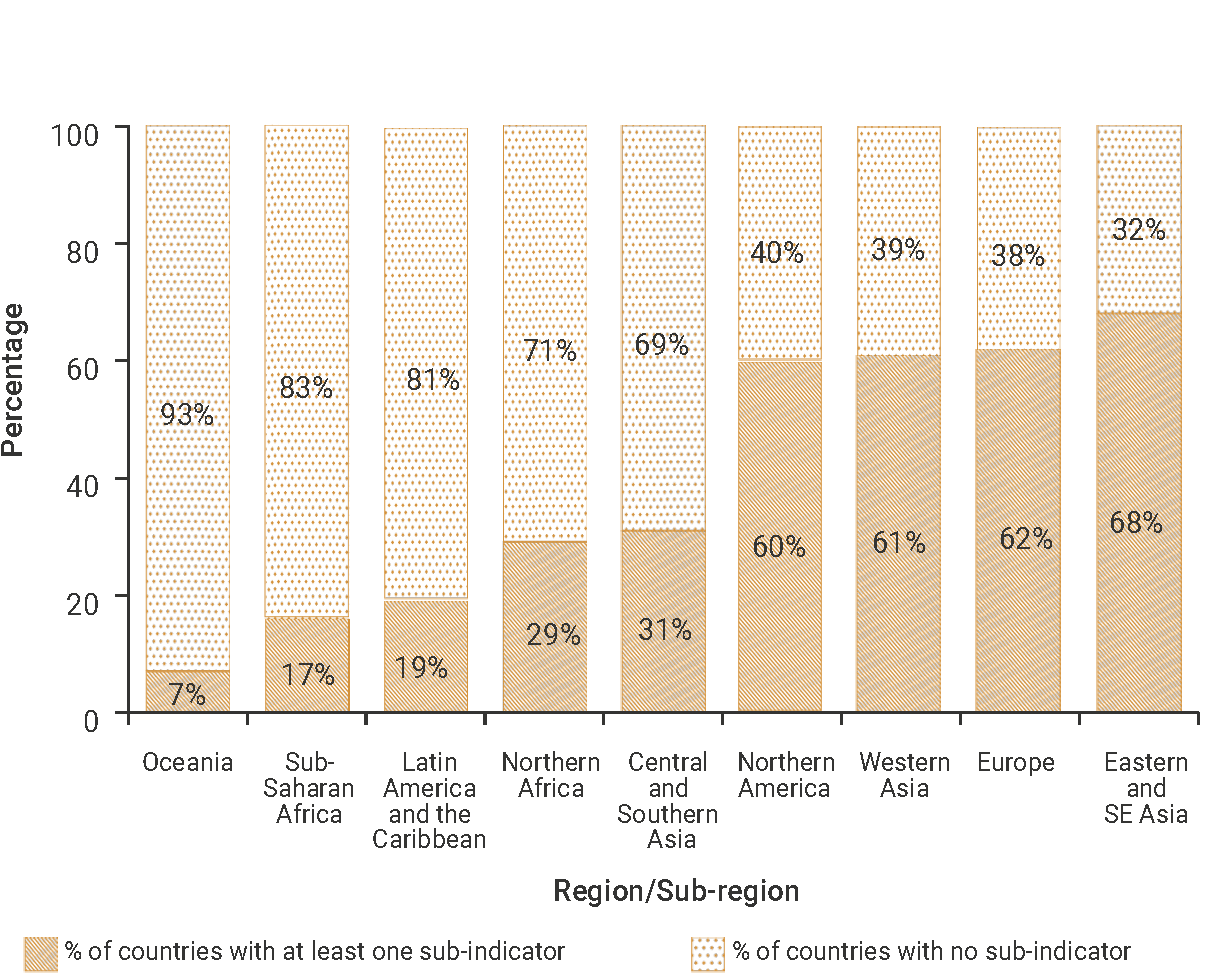

2. Data availability by region, SDG Global Database, as of 02 July 2025

3. Proposed disaggregation, links to policymaking and its impact

| Proposed disaggregation | Link to policymaking | Impact |

|---|---|---|

|

Number of companies publishing sustainability reports with disclosure by dimension, by level of requirement:

Applies to:

|

This disaggregation gives valuable information on the quality of the reports in relation to the achievement by companies of a range of sustainable development objectives. It distinguishes between a ‘minimum’ level and an ‘advanced’ level of requirement. This helps both governments and companies to monitor and control the compliance of company reporting with international reporting, standards as well as the level of reporting, to promote enhanced sustainability practices by companies (United Nations Conference on Trade and Development [UNCTAD] 2019). This disaggregation is consistent with the 10YFP (UN 2012; UNEP 2024c). |

Sustainability reporting offers an opportunity for businesses to communicate their efforts and actions towards decoupling consumption and production patterns from the use of natural resources. For example, increasing material and energy use efficiency, promoting the circular economy and goods durability. This reduces the pressures exerted by their activities on the environment (e.g. via emissions of pollutants, waste generation, dissemination of hazardous substances and chemicals, or biodiversity loss). It supports the mainstreaming of social considerations into their strategies and activities (e.g. the promotion of gender equality and decent working conditions, safety and health safeguards or social security schemes). It highlights the outcomes of their interventions. In doing so, it opens up new channels of communication for companies with various groups of stakeholders (e.g. institutions, citizens, consumer associations, NGOs and CSOs, or investors) and raises awareness. It also allows for the strengthening of relationships (e.g. via a regular newsletter, visits to production sites or forums) and may lead to new forms of partnerships (e.g. collaborative platforms or co-funding of projects with civil society or research institutions). Sustainability reporting contributes to the improved reputation of businesses, better legal compliance and fewer financial and technological risks or accidents. As a result, it boosts the access of corporates to new markets and helps upgrade competitive positions. With the growth in the number of investors that aim to pursue sustainability objectives, sustainability reporting has become a key instrument to access financial capital and to secure a collaborative socio-economic environment (OPN 2014; EC n.d.). |

|

Number of companies publishing sustainability reports with disclosure by dimension, by sustainability category:

Applies to:

|

This disaggregation tracks the distribution of published sustainability reports by sustainability disclosure categories. This is relevant information for monitoring which sustainability categories are well covered by sustainability reports and which are not. It can be used by policymakers as well by companies to point to the efforts that need to be undertaken to fill the identified gaps and ensure that all elements of sustainability are covered by sustainability reports in the future. This disaggregation is consistent with the 10YFP (UN 2012; UNEP 2024c). |

|

|

Number of companies publishing sustainability reports with disclosure by dimension, by company size:

Applies to:

|

This disaggregation helps policymakers and companies to differentiate the efforts made, both quantitively and qualitatively, by size of company to underline their reporting responsibility in relation to sustainable development (Metadata for indicator 12.6.1). This could result in incentives or the development and implementation of policies to encourage companies to do more for sustainable development. This disaggregation is consistent with the 10YFP (UN 2012; UNEP 2024c). |

Corporate sustainability reporting of all company sizes is essential for promoting responsible practices, transparency and accountability of businesses (UN Global Compact). Evidence shows that it contributes to their financial stability and good governance. It also strengthens people's trust in companies and forces them to do more for the quality of the environment, with convincing results in terms of natural resource management, biodiversity protection, GHG mitigation, and improving public health (UNEP 2019c; Global Reporting Initiative [GRI] 2024). |